UK DIY News

BMBI Notes Downward Trend in Builders Merchant Sales in Q4 2025

Figures released in the latest BMF Builders Merchants Building Index (BMBI) confirm the challenges facing the builders’ merchants sector, showing a further decline in sales performance in the final quarter of the year, following the downward trend seen in the third quarter.

The Q4 downturn marks the end of a disappointing second half of the year, erasing much of the initial growth seen in the first two quarters of 2025. However, 2025 still concluded with a value growth of +0.5%, a testament to the dedication and hard work by both merchants and tradespeople.

Quarter 4 2025 v Quarter 4 2024

Looking at the quarter as a whole, year-on-year total value sales in Q4 2025 were lower than the same period in 2024. With no difference in trading days between the two periods, Total Builders Merchants value sales in Q4 2025 were -1.2% lower than Q4 2024. Volume sales were down by -2.9%, but prices increased by +1.8%.

Value sales increased in seven of 12 product categories, led by one of the smallest categories, Miscellaneous (+6.4%). Timber & Joinery Products, the second largest category, increased by +1.8%, outperforming the total market, but the largest category, Heavy Building Materials, at -3.9%, recorded the weakest performance.

Quarter 4 2025 v Quarter 3 2025

Value sales in Q4 2025 were weaker than in the third quarter of the year. Like-for-like value sales (adjusted to remove the impact of trading days) were -9.0% lower than in the previous quarter. Like-for-like volume sales were down by -13.1%.

With four fewer trading days in Q4 2025, unadjusted value sales for the Total Builders Merchants Market were -14.6% lower than in Q3 2025. Volume sales declined by -18.5%, but prices rose by +4.8%.

Ten of the 12 product categories sold less by value, with Workwear & Safetywear (+6.0%) and Plumbing, Heating & Electrical (+4.7%) the only categories to sell more. Timber & Joinery Products (-13.3%) performed better than Total Builders Merchants, but the largest category, Heavy Building Materials, at -16.2%, was one of the poorest performers.

Full year vs last year

January-December 2025 v January-December 2024

With one less trading day in 2025, Total Builders Merchants unadjusted value sales for the full year were +0.5% higher in 2024, with volume increasing by +1.5% and average price down by -1.0%.

The largest category, Heavy Building Materials, ended the full year with a value decline of -0.5%. Volume was up by +1.2%, but the average price was down by -1.7%. The main contributors to these declines were blocks, insulation, plasterboard, and roofing products. Aggregates, bricks, and cement were key areas of growth.

However, Renewables & Water Management was the best performing category for the year, with value sales increasing by +5.7%. Plumbing, Heating & Electrical also had a positive year, up by +1.8%, with boilers, tanks, heating equipment, and heat pumps being areas that contributed to growth in 2025.

Emile van der Ryst, Key Account Manager – Trade & DIY at NiQ GfK, said:

“Although 2025 recorded a value growth of 0.5%, the shift in the quarterly value growth trend compared to 2024 is a genuine concern. Both Q1 and Q2 2025 were positive at +0.7% and +2.6% respectively. However, there have now been two consecutive quarters of decline, with Q3 down by -0.3% and Q4 decreasing further to -1.2%. 2026 has continued on this challenging path, not helped by the weather in January and February. There is hope that 2026 could improve as the year progresses, but for this to happen there would need to be drastic changes in some of the global and local issues currently experienced.”

John Newcomb, CEO of the BMF, said:

“Providing building materials for housing—whether for new builds or RMI – is a central aspect of our sector, but with fewer people moving home or entering the housing market, demand across the supply chain remains subdued. It is difficult to foresee significant growth in these markets without a return of consumer confidence, which government support for first-time buyers could help foster. Unfortunately, a new factor has now emerged, as the Middle Eastern conflict is almost certain to cause higher inflation, delaying a previously expected interest rate cut.”

Click here for more information on the quarterly results

Disappointing December rounds off a tough trading year

The latest Builders Merchant Building Index (BMBI) report reveals builders’ merchants’ like-for-like value sales for Q4 2025, adjusted to remove the impact of trading days, were -1.2% lower than Q4 2024. Like-for-like volume sales were down -2.9%.

With no difference in trading days, unadjusted Q4 total value sales were also down -1.2% year-on-year. Volume sales fell -2.9% while prices rose +1.8%. By value, seven of the twelve categories sold more with Miscellaneous (+6.4%) ahead of the rest. Of the two biggest categories, Timber & Joinery Products (+1.8%) performed better than Total Builders Merchants, and Heavy Building Materials (-3.9%) was the weakest category.

Like-for-like sales for Q4 2025 were -9.0% lower than Q3 2025, with like-for-like volume down -13.1%. With four less trading days in Q4, total unadjusted quarter-on-quarter value sales were -14.6% lower, with volume down -18.5% and prices up +4.8%. Only two categories sold more, Workwear & Safetywear (+6.0%) and Plumbing, Heating & Electrical (+4.7). Timber & Joinery Products sold -13.3% and Heavy Building Materials -16.2% less. Seasonal Landscaping (-31.7%) was the weakest.

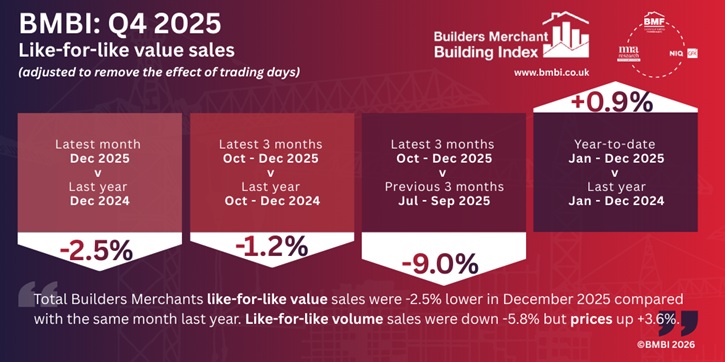

December 2025 like-for-like sales were -2.5% lower than the same month the previous year. Like-for-like volume sales decreased -5.8%. With one additional trading day in December 2025, unadjusted total value sales were up +3.3% year-on-year. But volume sales were -0.3% lower and prices up +3.6%. By value, ten categories sold more with Renewables & Water Saving (+16.7%), Kitchens & Bathrooms (+9.8%) and Plumbing, Heating & Electrical (+9.8%), the standout categories. Of the big product categories, Timber & Joinery Products sold +8.6% more, while Heavy Building Materials (-0.5%) and Landscaping (-5.1%) both sold less.

Month-on-month, December’s like-for-like value sales were -18.2% down compared to November, with volume sales down -20.6%. With two less trading days in December, unadjusted total value sales were down -26.3%. Volume sales were down -28.5% and prices were up +3.1%. All categories sold less by value, but Services (-13.8%) fell by less than other categories. Of the biggest categories, Timber & Joinery Products fell -26.1%, Heavy Building Materials -28.3%, and Landscaping -31.3%.

Year-to-date like-for-like value sales for January to December 2025 were +0.9% up on 2024. Like for like volume sales increased +1.9%. With one less trading day in 2025, total unadjusted sales were +0.5% higher; volumes were up +1.5% while prices eased -1.0%.

Mike Rigby, MD of MRA Research who produce this report, said: “The UK economy grew by just +0.1% in Q4 2025, according to the ONS, as business and consumer confidence nosedived ahead of the Autumn budget, ensuring a subdued end to the year. But ONS’s construction output data recorded a bleaker and more disappointing end for construction with Q4 output shrinking -2.1% compared to Q3. Private new housing (-3.6%) the main negative contributor.

“The Construction Products Association (CPA) duly downgraded its forecast construction output for 2026 from +2.8% to +1.7% and downgraded its forecast for private housebuilding from +4.0% to +1.5%. Private housing RMI was revised down to -1.0%.

“With unemployment (5.2%) climbing to its highest rate in five years (16.1% for 16–24-year-olds – the highest in 10 years), and a New Year which has seen both non-stop political crisis and rain every day, the prime minister has likely reached saturation point for just about everything.

“But it’s not all bad news. Inflation, measured by the Consumer Prices Index (CPI), rose by +3.0% in the 12 months to January 2026, down from +3.4% in the 12 months to December 2025, and some economists are forecasting a fall to the Bank of England’s target rate of +2% sometime this year. That could encourage the Bank to cut interest rates more often and by more than expected, which could encourage investor, business and consumer spending.

“The Chancellor, Rachel Reeves, is set to deliver the Spring Statement early in March, amid a surprise record-breaking budget surplus of £30.4bn in January 2026 and she’s been very clear about not delivering any tax rises – in the interests of stability and certainty. These are two qualities the construction industry and its supply chain desperately need. Without that, it’s difficult to see how 2026 will not be more of the same.”

Set up and run by MRA Research, the BMBI – a brand of the Builders Merchants Federation – is a monthly index of builders’ merchant sales, and the most reliable, up-to-date proxy for Repair, Maintenance, and Improvement (RMI) activity in the UK. The index is based on actual sales from NiQ GfK’s Builders’ Merchant Point of Sale Tracking Data, which captures value sales out to builders from generalist builders’ merchants, accounting for 88% of total sales from builders’ merchants throughout Great Britain. An in-depth review, which includes commentary by sector experts, is produced each quarter.

Source : BMBI

Image : BMBI

Insight provides a host of information I need on many of our company’s largest customers. I use this information regularly with my team, both at a local level as well as with our other international operations. It’s extremely useful when sharing market intelligence information with our corporate office.

Don't miss out on all the latest, breaking news from the DIY industry