UK DIY News

Kingfisher Q1 Boosted by Screwfix and Iberia; Guidance Maintained

- Kingfisher on track to deliver full year guidance

Q1 Highlights

- Underlying± LFL (0.7)% vs. strong prior year comparator. Total sales including marketplace GMS +0.8%(3)

- Core categories resilient, despite late start to spring impacting footfall

- Market share gains at Screwfix and in Poland. France and Spain in line. B&Q more exposed to seasonal

- Strong momentum from strategic growth drivers

- Trade sales grew +17% ex-Screwfix. Group trade sales penetration 31%

- E-commerce sales increased +14% ex-Screwfix. Group e-commerce penetration 22%. Marketplace GMV(3) grew +39% to £163m

- Opened 5 stores including the first standalone TradePoint

FY 26/27 Guidance

- On track to deliver full year guidance: expect FY 26/27 adjusted PBT of c.£565m-£625m and free cash flow of c.£450m-£510m

- £300m share buyback ongoing

Thierry Garnier, Chief Executive Officer, said:

"We delivered a resilient start to the year, executing well and gaining market share against a soft market backdrop. Sales including marketplace grew +0.8%, with core categories proving resilient - even as a late start to spring impacted footfall and seasonal demand. E-commerce and trade sales both delivered double-digit growth, underlining the momentum in our key growth drivers.

While mindful of the consumer environment, we remain absolutely focused on delivering our strategy, disciplined gross margin and cost management, and consistent shareholder returns. We are confident in achieving our full-year guidance and are well positioned to capitalise on the attractive long-term growth opportunities across our markets."

Q1 trading by banner | Sales 2026/27 (£m) | % change reported | % change cc* | % change |

- B&Q | 1,025 | (3.0)% | (3.1)% | (4.1)% |

- Screwfix | 712 | +5.5% | +5.4% | +4.1% |

UK & Ireland | 1,737 | +0.3% | +0.2% | (0.9)% |

- Castorama | 511 | +1.8% | (1.5)% | (1.1)% |

- Brico Dépôt | 479 | +1.1% | (2.2)% | (3.1)% |

France | 990 | +1.4% | (1.8)% | (2.1)% |

Poland | 457 | +3.3% | +0.9% | (0.2)% |

- Iberia(4) | 109 | +10.2% | +6.6% | +6.6% |

- Screwfix France & Other(5) | 7 | +62.9% | +58.1% | n/a |

Other International** | 116 | +12.6% | +9.0% | +7.8% |

Total Group** | 3,300 | +1.4% | (0.0)% | (0.9)% |

Underlying± excluding calendar impact (2) |

|

| (0.7)% | |

±Underlying sales growth refers to sales excluding calendar and leap year impact. In Q1 the calendar impact is (0.2)% (LFL sales (0.9)% + 0.2% = underlying LFL of (0.7)%(2)).

*Constant currencies.

**Other International and Total Group figures exclude Romania. Total Group including Romania sales are (0.4)% on reported currency and (1.9)% on constant currency. On 2 May 2025, the Group completed the divestment of its 100% equity interest in Brico Dépôt Romania.

All commentary below is in constant currency.

UK & Ireland

- Market declined low single digits(6).

- B&Q - total sales including marketplace GMS (1.3)%. LFL (4.1)% against strong prior year comparator and a late start to spring impacting footfall, seasonal sales and related purchases of core categories. Big‑ticket reflective of a soft bathroom market, partly offset by strength in new kitchen ranges. Strong progress in e‑commerce with sales +16% and Marketplace GMV +29%. E-commerce penetration reached 19%. One store opened.

- TradePoint - LFL (1.6)% against a strong prior year comparator and fewer outdoor projects due to weather. Continued active recruitment of trade sales partners. First standalone TradePoint opened, targeting trade customers working in dense urban areas.

- Screwfix - Significant market share gains(6) driven by volume and transactions. LFL +4.1% based on strong core performance (c.85% of total), supported by continued momentum from our app-based rewards programme alongside ultimate convenience delivered through Screwfix Sprint and Click & Collect.

France

- Market declined low single digits(6) as consumer savings rates remain elevated.

- Castorama - LFL (1.1)%, a third quarter of sequential improvement. Momentum driven by core following successful range reviews, stores previously right-sized and revamped and good seasonal sales. Big-ticket impacted by a subdued project environment. Continued growth in e-commerce +8.7% with penetration reaching 10%, supported by marketplace growth. Trade penetration grew from 1% to 8%. Completed three right-sizes and two revamps.

- Brico Dépôt - LFL (3.1)% with big-ticket impacted by a subdued project environment. Trade sales grew +28%, driven by the continued strengthening of our trade proposition, and penetration now stands at 16%. One store was opened in the quarter. First franchise store opened in May.

Poland

- Market declined low single digits(6).

- Outperformed the market. LFL (0.2)% with resilient demand in core growing +2%. Seasonal impacted by cold temperatures. Big-ticket reflective of weakness in bathroom market, partly offset by market share gains in kitchens. Continued momentum in e-commerce sales +41% and trade sales +13%. Trade penetration stands at 28%. One store opened in April.

Other International

- Iberia - strong LFL +6.6% led by core and seasonal categories. Trade sales growth +44% with good uptake of the loyalty programme.

- Screwfix France - continued progress with store LFL growth of +55% supported by strong customer recruitment and growing share of wallet as trade customers become more familiar with the Screwfix proposition. One store opened.

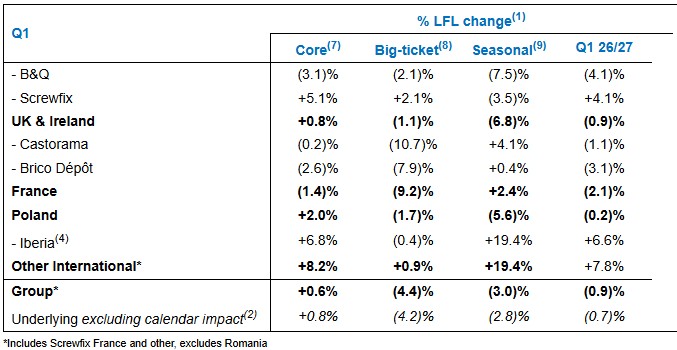

LFL sales by category

Core (65% of sales): resilient performance across banners, led by strong performance of Screwfix, partly offset by softer sales at B&Q with lower footfall related to a late start to spring.

Big-ticket (15% of sales): subdued big-ticket market, particularly in the bathroom category, partially offset by strong kitchen performance at B&Q and in Poland driven by recent range reviews. Bathroom range reviews are planned in 2026.

Seasonal (20% of sales): due to a late start of spring in UK and Poland, partially offset by growth in France and Iberia.

Guidance for FY 26/27

We expect to deliver:

- Adjusted PBT in the range of approximately £565m-£625

- Free cash flow in the range of approximately £450m-£510m

Key Assumptions:

- Space: sales impact of c.+1%, mainly from Screwfix UK & Ireland, B&Q and Castorama Poland

- Net finance costs: c.£105m (FY 25/26: £91m)

- Adjusted effective tax rate: c.26% (FY 25/26: 26%)

- Capex: c.£400m (FY 25/26: £388m)

- £13m non-recurring 2025/26 losses

Footnotes

(1) LFL (like-for-like) sales growth represents the constant currency, year-on-year sales growth for stores that have been open for more than one year.

(2) Underlying growth refers to LFL sales excluding calendar impact: Calendar impact represents the impact of the annual calendar shift on LFL sales growth due to different days of the week falling into or out of the current period compared to the prior period. For example, historically, higher trading is seen on a Friday and Saturday as compared to a Sunday. This includes the impact of national public holidays falling on different days of the week compared to the prior period. The estimated impact of the annual calendar shift on Q1 26/27 LFL sales is (0.2)%.

(3) Gross merchandise sales (GMS) refers to the transaction value (excluding VAT) from the sale of products including third-party e-commerce marketplace vendors. Marketplace GMV is the total transaction value (including VAT) from the sale of products supplied by third-party e-commerce marketplace vendors. What is recorded in revenue is the commission take rate which is c.10-15% of GMV.

(4) Brico Dépôt Spain and Portugal.

(5) Screwfix France & Other consists of the consolidated results of Screwfix France and wholesale agreements.

(6) Market numbers based on, GfK, BRC (British Retail Consortium) and Barclays for the period of February 2026 to April 2026; GfK, Banque de France for France for the period of February 2026 to March 2026; GFK for Poland for the period February 2026 to April 2026; AECOC for Spain for the period of February 2026 to April 2026.

(7) Core category sales include the sales from non-seasonal products across all our categories, other than big-ticket sales.

(8) Big-ticket category sales include the sales from kitchen, bathroom & storage products.

(9) Seasonal category sales include the sales from certain products within our outdoor, electricals, plumbing, heating & cooling (EPHC) and surfaces & décor categories.

Source : Kingfisher plc

Image : Kingfisher plc

I find the news and articles they publish really useful and enjoy reading their views and commentary on the industry. It's the only source of quality, reliable information on our major customers and it's used regularly by myself and my team.

Don't miss out on all the latest, breaking news from the DIY industry