UK DIY News

Pepco: Resilient Annual Trading Across All Brands

The fast-growing pan-European variety discount retailer, Pepco Group, owner of the PEPCO and Dealz brands in Europe and Poundland in the United Kingdom (UK), today filed, with Companies House, its annual Statutory Accounts for the 52 weeks ending 30 September 2020[1].

Strategic Progress

- 327[9] (+12%) net new stores opened, closing the year with 3,021[2] stores in 15 countries.

- Successfully opened the first multi-price (PEPCO) stores in the strategically important markets of Italy and Serbia the first Western European and non-EU country respectively*.

- Accelerated roll-out of the price-anchored (Poundland & Dealz) brand opening 43 stores in Poland & Spain.

- Proposition development continued, including further extension of multi-price to all remaining categories in Poundland / Dealz. Acquisition of Fultons Frozen Foods completed in October to further support roll-out of chilled and frozen proposition in the UK.

- Commenced a store refresh programme in PEPCO and Poundland. Initial 84 and 52 stores, converted respectively with further 700 store targeted in FY21.

- Preparations commenced for further western European expansion for PEPCO to Spain in second half of the current financial year, following detailed research on the market opportunity.

- Strengthened balance sheet through pro-active and permanent improvements to working capital.

Financial highlights

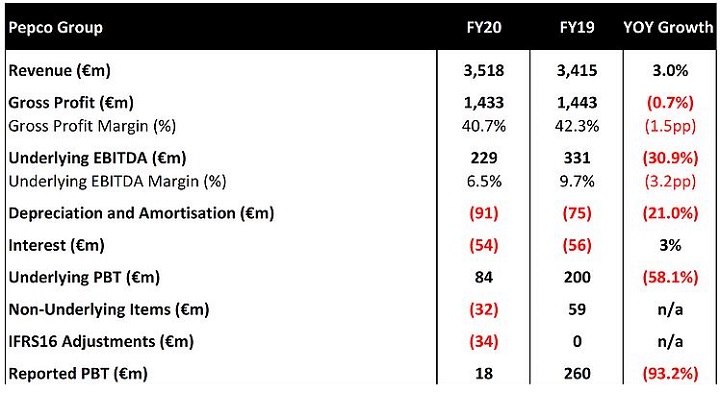

- Sales increase of 3.0% to €3.5bn despite significant Covid impact, primarily in Q3 LFL. More than offset by resilient LFL[8] performance outside of these periods and store openings, a trend which we continued into Q1 F21 as reported on the 27th January[3]

- Underlying EBITDA[4] €229m (FY19: €331m). Reduction primarily related to temporary Covid-related store closures, particularly in Central Europe, from April to June 2020. In the five months to the end of February[5], pre the impact of Covid-19, underlying EBITDA grew strongly (+18% year on year)

- Cash generated by operations[6] of €405m (FY19: €236m) driven by new store-led sales growth and effective working capital management as part of our response to Covid-19. Year-end net debt[7] of €328m (FY19: €461m).

Outlook

- Whilst the near-term consumer environment is likely to continue to be impacted by Covid related shopping restrictions, we remain confident about our long-term growth strategy.

- Consistent with FY20 investment to support future growth will continues with 400 stores planned to open in the current financial year and initial implementation of group-wide Oracle ERP system.

Commenting on the results, Andy Bond, CEO of Pepco Group, said:

“We again made good progress in the last year delivering the convenience and market leading value that our customers are seeking and advancing our pan-European growth strategy, despite a turbulent trading environment. Our robust profit and cash performance clearly demonstrates the strength of each of our retail brands and customer offers together with our resilience to short-term Covid disruption.

With a strengthened proposition and more customers than ever across Europe being attracted to the discount sector we believe that our future growth opportunity is now greater than a year ago. We now view our addressable market as being the entirety of Europe and having entered Italy and Serbia ‒ our first Western European market and non-EU country respectively ‒ we will also launch PEPCO in Spain in later in 2021, having identified a significant opportunity there after extensive due diligence.”

“We anticipate that the consumer backdrop will remain challenging in the short-term. However, with our strong financial base and established growth strategy within a structurally advantaged discount retail segment, we remain confident about our long-term prospects for continued growth across Europe.”

FY20: Covid-19 Impact context

While, consistent with other retailers, initially managed during February as a potential supply issue, Covid-19 impacted consumer demand for all retail brands within the Group with governmental restrictions being introduced across CEE from mid-March, Spain from 15 March, the UK from 23 March and Ireland from 27 March 2020.

As it did not qualify as a retailer of essential products, PEPCO was our most impacted brand. In the closing week of the quarter to the end of March, PEPCO traded from 856 (44%) of its 1,930-store footprint with the entire portfolio closed in seven countries including Czechia, Slovakia and Romania. Trading in Poland was limited to stores outside of shopping malls while stores in Hungary were only permitted to trade between 9 am and 3 pm each day.

These restrictions, combined with the need for social distancing across all markets and the reluctance of some customers to venture out of their homes, meant PEPCO traded for a four-week period immediately post lockdown at c. 15% of its expected sales levels.

Poundland qualifies as a retailer of essential products and consequently experienced an initial benefit from customer stockpiling of cleaning, healthcare and food products. However, the Covid-19 lockdown led to the voluntary temporary closure of 130 stores in March 2020. The remaining c. 700 stores traded through significantly reduced visitor numbers, particularly in shopping centres and high street locations, at c. 60% of expected sales levels for a period of four weeks.

Our financial performance in the five months to the end of February 2020 continued its recent profile of strong revenue and profit growth. As outlined below, our unaudited performance in that period recorded 14.4% revenue growth, benefiting from both continued store growth and 5.0% Group level like for like, with LFL growth achieved in each of our segments. Continued scale and efficiency-led cost leverage contributed to year-on-year EBITDA growth of 18%

Results – Full Year

The Group generated in excess of €3.5bn of sales in the period, growing year on year by 3.0%, driven predominantly by store growth with 327 net new stores opened in the period under review (12% year-on-year growth). LFL sales decreased year on year by 5.2%, reflecting the impact of strict Covid-19-related lockdowns on footfall across all the territories we operate in.

The Group generated underlying EBITDA of €229m and underlying profit before tax of €84m in the period, driven by PEPCO store expansion-led profit growth. The Group remained profitable despite the impact of Covid-19 in the second half of the year, although underlying EBITDA declined by €102m (-31%) year on year. The Group delivered an underlying EBITDA margin of 6.5%, a reduction of 3.2pp year on year.

Reflecting the impact of Covid in the final seven months of the financial year, we delivered strong underlying EBITDA growth (+18% year on year) in the five months to the end of February, pre the impact of Covid-19.

Finances

Despite the impact of Covid-19, the Group generated €405m operating cash flow in the period, driven by new store-led sales growth and effective working capital management as part of our response to Covid-19, which included stock cancellations or deferrals, renegotiations of payment terms with key suppliers and reductions in operating costs during the lockdown periods.

Capital expenditure (before the impact of IFRS 16 accounting adjustments) increased by €28m in FY20 to €163m. The key drivers included our ongoing strategic investment in new store openings, individual store expansions and relocations (€71m) as we continue to expand the business. Furthermore, we also invested in new infrastructure to underpin our anticipated growth including IT and systems (€35m) and warehousing (€33m).

New Store Expansion

Despite the trading challenges, we maintained our store expansion strategy during the Covid-19 affected period, reflecting the resilience and strength of the business, opening 327 stores. We exited the FY20 period under review with 3,021 stores across 15 countries.

We expanded our PEPCO store estate by 296 stores in the year under review (16% growth year on year), including entering the Western European market with five stores in Italy at the year end. These initial Italian stores have traded ahead of our internal expectation since their opening. Evidencing the strength of our proposition relative to incumbent competition, both customer numbers and average transaction values are delivering measurable premiums to our business plan.

Recognising this performance, we envisage operating from over 20 stores in Italy at the end of the year ending 30 September 2021 and in spring 2021 will open our first stores in Spain, where again the PEPCO proposition has been researched strongly.

In our Poundland Group segment, our expansion of the Dealz brand continued, with 31 openings in Poland, where the brand’s recovery from Covid-19 has been particularly strong, and 12 in Spain, exiting the year with 96 Dealz stores in mainland Europe as well as a further 69 in ROI. Recognising the maturity of the UK market and in line with our strategy to optimise the Poundland store estate in the UK, our UK portfolio remained broadly flat.

Stores – Existing

Both PEPCO and Poundland are now progressing a significant proposition refresh programme that will be introduced progressively, on a store-by-store basis, to benefit most stores over the next two to three years.

In PEPCO this is centred on the opportunity to better balance space between apparel and general merchandise, without any reduction in range. On each store refit we will also look to divide the store on a right hand/left hand basis rather than the current front/back basis. Particularly in new markets, where the brand will be less well known, this will make a greater breadth of the proposition visible from the entrance of the store, encouraging visit. It is anticipated that over 700 stores will be refreshed during the current financial year following the successful introduction in the period under review.

A similar programme within Poundland will be rolled out to over 400 UK stores during the next two years centred on the introduction of a chilled and frozen range of products to complement our existing grocery offer. Following extensive research with our customers and having extended our price hierarchy, chilled and frozen products were by far the most commonly referenced category that our customers wished to buy from us.

The same programme will also re-lay each store to the further benefit of customers and colleagues. Store layouts will be adjusted to reflect our latest view on optimal adjacencies and operational efficiency will be enhanced by, for example, reviewing the balance between manned and self-scan checkouts based on our accumulated learning.

Each brand is also constantly seeking to refresh its respective proposition by trialling potential new categories based on customer research. As examples in the forthcoming year, Poundland will trial a beer, wines and spirits offer and a healthy living range including “free-from” products and PEPCO will test a range of baby-centric FMCG products such as nappies and wipes.

Operating Costs

In PEPCO operating costs, excluding depreciation, amortisation and non-underlying costs, grew in line with the increased store base by 17.6% and increased by 300bps on a percent to sales basis as lower like-for-like sales impacted operational leverage.

In the Poundland / Dealz segment operating costs were 2.0% higher versus the previous year with the business continuing to drive operating cost efficiencies in line with the Group’s strategy focusing principally on store rent and programmes to reduce logistics and head office costs. We also benefitted from Covid-19-driven governmental schemes such as business rates relief. However, these cost reductions were offset by increases in the cost bases of the Dealz businesses as we continued to expand through new store openings.

Outlook

We remain committed to continuing our investment in both new and existing stores, planning to open stores in PEPCO at slightly above our recent historic rate of c. 300 per year and increasing our Dealz store roll out in mainland Europe in addition to refreshing over 1000 existing stores in the current financial year.

Looking forward, it is likely that consumer demand for discount retailing will increase in a period of prolonged economic uncertainty and we are extremely well placed to take advantage of this trend. We remain confident that we have the vision, the strategy and the business model to continue to deliver attractive long-term sales and profit growth.

Source : Pepco

Image : nrqemi / Shutterstock.com

I find the news and articles they publish really useful and enjoy reading their views and commentary on the industry. It's the only source of quality, reliable information on our major customers and it's used regularly by myself and my team.

Don't miss out on all the latest, breaking news from the DIY industry