UK DIY News

Topps Tiles Outperforms Softer Market; Makes Good Strategic Progress

Topps Tiles Plc ("Topps Group", the “Company" or the “Group”), the UK's leading tile specialist, announces its unaudited consolidated interim financial results for the 26 weeks ended 28 March 2026.

Strategic and Operational Highlights:

The Company has made significant progress against Mission 365 and the priorities for the year that we laid out in December 2025.

- Focus on profitability: We continue to expand gross margin and have implemented 3 major self-help cost initiatives aimed at accelerating progress to 8%+ PBT margin. This approach counteracts structural headwinds, creates a simpler and more flexible model and positions Group for sustainable long-term growth to support Mission 365 ambition.

- Topps Group has outperformed the RMI market1, underpinned by progress in key strategic areas:

- Delivering trade growth: Trade mix increased to 74.6% of revenue across the group, delivering 4.1% growth in Trade (ex-CTD), with Pro Tiler growing c.20% year on year, supported by H1 expansion of own-brand, PremTool.

- Accelerating digital: Online revenue rose to c.21% (H1 2025: c.18%). Positive results from new customer engagement platform, improved marketing efficiency, website conversion rates and customer offers including live stock visibility. System modernisation rollout, including new tills and ERP upgrade, underway and on track.

- Driving sales excellence: Extended Topps Tiles brand to capture customer growth in value segment and consolidated Tile Warehouse into Topps, simplifying offer to customers, and leveraging Topps Tiles’ greater brand penetration and better cost to serve. New category “hard surface” extensions up 7% year on year. - Integrating acquisitions to drive sustainable profit: CTD loss improved by £0.6m year-on-year and on track to be profitable in the second half. Fired Earth exceeding business case expectations and already profitable in the period. Fired Earth range in 4 countries outside of the UK via branded stockists, opening up new growth options.

- New CFO: Caroline Browne joins on 26 May 2026.

Financial Highlights:

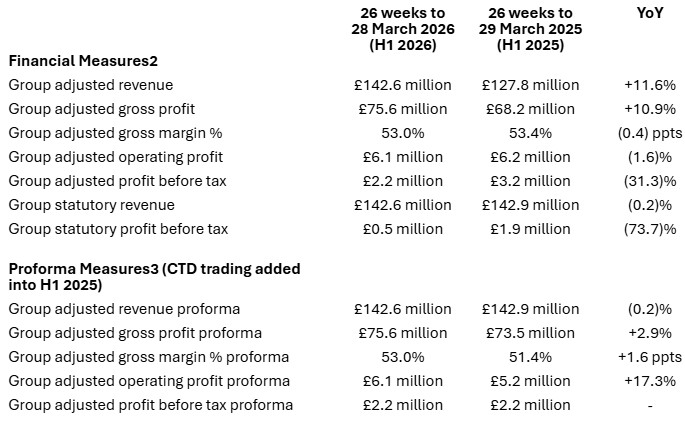

The financial impact of CTD was excluded from adjusted2 measures in FY 2025. In FY 2026 CTD is included in adjusted measures. For comparability, proforma3 financial measures are shown below with CTD trading included in H1 2025.

Financial Summary:

- Revenue performance robust, and ahead of the market, in a challenging environment. Adjusted revenue of £142.6m up 11.6% year-on-year driven by inclusion of £12.3 million of CTD revenue in H1 2026. Proforma adjusted revenue is marginally down 0.2%.

- Adjusted gross margin down 0.4 ppts, driven by mix due to margin dilutive CTD business included in H1 2026.

- Proforma adjusted gross margin up 1.6 ppts with strong margin growth in Topps Tiles.

- Proforma adjusted operating costs up 1.8% with management driven cost savings largely offsetting inflation driven cost increases.

- Self-help cost saving and profit driving initiatives will further underpin profit delivery in the second half.

- Proforma adjusted operating profit up 17.3% given solid gross margin growth and tight operating cost management.

- Adjusted profit before tax of £2.2 million down £1.0 million versus prior year, however, flat at £2.2 million on a proforma basis, given CTD trading was a loss of £1.0 million in H1 2025.

- Statutory revenue (including CTD in both years) of £142.6m marginally down 0.2% year-on-year.

- Statutory profit before tax £0.5 million (H1 2025: £1.9 million) including the impact of store impairment, one-off property related closure costs, CTD residual one-off and non-recurring costs and management succession.

- Balance sheet remains robust, with adjusted net debt4 of £3.1 million at the period end (H1 2025: net debt £1.2 million), and £30 million banking facility committed until October 2027.

- Interim dividend of 1.0 pence declared in line with policy.

Current Trading and Outlook

- Topps continues to outperform softer market:

- Topps Tiles like-for-like revenue in the first seven weeks of the second half has returned to positive, up 0.6% which, encouragingly, is a step up versus Q2 2026 (down c. 2%). CTD stores like-for-like revenue also up 3.0% in the first seven weeks of the second half.

- We continued to see strong growth in online across the first seven weeks of the second half, including record revenue weeks achieved in Pro Tiler. - Significant progress has been made against our strategic priorities including resetting our cost base and consolidating Topps as the market leader in tiles. While the macro and geopolitical external environment remains challenging, the Group benefits from a resilient and well-diversified supply chain. The self-help measures we have implemented along with a continued focus on productivity, efficiency and cost discipline mean we expect to deliver profit upside in the second half relative to the first half and deliver modest year-on-year profit growth in line with market expectations.

Commenting on the results, Alex Jensen, Chief Executive said:

“Topps remains a market outperformer despite a softer backdrop of weaker consumer sentiment, geopolitical uncertainty and the cumulative impact of cost inflation. We are making good progress in delivering our strategic agenda, including a programme of self-help measures weighted towards the second half, and we are accelerating growth in digital, trade and category extensions. These actions are designed to support modest year on year profit growth and provide a stronger financial platform for 2027, positioning the Group for long-term sustainable profit growth.”

Notes

1 Market performance as defined by Barclays "UK Consumer Spend Report" for Home Improvements & DIY which was +0.4% in October 2025, -2.0% in November 2025, -5.4% in December 2025, -2.4% in January 2026, -3.1% in February 2026 and -2.5% in March 2026, averaging c. -2.5% over this period.

2 Adjusted items are Alternative Performance Measures which are used by Group management to plan for, control and assess the performance of the Group. These measures are not defined by IFRS and therefore a reconciliation between each APM and the nearest IFRS measure is presented in the most recent Annual Report and Accounts. Topps Tiles like-for-like revenue is defined as sales from Topps Tiles stores that have been trading for more than 52 weeks and online sales made through the Topps Tiles brand (only). Adjusted sales and profit metrics exclude the impact of items which are either one-off in nature or fluctuate significantly from year to year, described in the Financial Review section of this document.

In the prior year FY 2025 period, the performance of CTD was fully excluded from adjusted metrics due to the ongoing disruption caused by the CMA investigation. In FY 2026, CTD is now included in the adjusted measures which skews comparability year-on-year.

3 The proforma financial measures add CTD ‘trading’ back into the H1 2025 base to provide a comparison of performance with CTD included in both the H1 2026 and H1 2025 financial periods. (For comparability, just the trading element of CTD has been added back into H1 2025, not the one-off acquisition, legal and advisor fees relating to the CMA investigation).

4 Adjusted net debt is defined as bank loans before unamortised issue costs, less cash and cash equivalents, as at the balance sheet date. It excludes lease liabilities under IFRS 16.

Source : Topps Tiles plc

Image : Topps Tiles plc

Insight DIY always publishes the latest news stories before anyone else and we find it to be an invaluable source of customer and market information.

Don't miss out on all the latest, breaking news from the DIY industry