UK DIY News

Dunelm Sees Continued Strong Growth

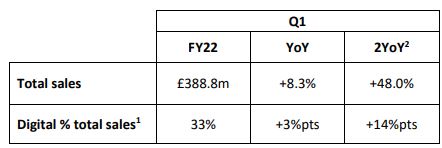

Dunelm Group plc ("Dunelm" or "the Group"), the UK's leading homewares retailer, reports on trading for the 13-week period ended 25 September 2021.

1) Digital includes home delivery, Click & Collect (or Reserve & Collect before October 2019) and tablet-based sales in store.

2) 2YoY represents performance against the comparable period in FY20.

Continued strong growth across the total retail system and market share gains

Total sales in the first quarter increased by 8.3% against a very strong comparative period in FY21, when sales grew by 36.7%. This strong performance was mainly driven by the positive customer response to our Summer Sale in July (which was postponed from the fourth quarter of FY21), improved product availability and some popular new ranges in our furniture categories.

Given the strength of the comparative Q1 FY21 period, which benefited from some pent-up demand following store closures during the first national lockdown, we are pleased to have grown sales across the total retail system during the quarter, with digital sales growing at 20%. This strong performance demonstrates the strength of our integrated offer, providing customers with an attractive digital proposition, combined with local, friendly and convenient in-store shopping experiences.

The data we receive from GfK shows that we continued to outperform the homewares market(3) and gained further market share in each week of the quarter.

3) Based on management’s estimates using weekly GfK homewares market data.

Robust gross margin

Gross margin in the first quarter decreased by 10bps compared to Q1 FY21, reflecting the Summer Sale timing impact, largely offset by a higher mix of full price sales and sourcing gains to offset anticipated cost price increases.

We expect gross margin for the first half to be flat to slightly positive compared to H1 FY21, noting that Q2 FY21 was impacted by store closures. As previously guided, we anticipate gross margin for the full year will be c.50-75bps lower than FY21, reflecting that the second half is expected to include both a Winter and Summer Sale.

Financial position

At 25 September 2021, the Group had net cash of £209m (FY21 Q1: £175m) and access to £175m of approved banking facilities which remain unutilised. The previously announced special and FY21 final ordinary dividends, totalling £178m, will be paid out during the second quarter(4).

Inventories at the end of the period were £168m (FY21 Q1: £136m; FY20 Q1: £161m), with good levels of availability across most of our product categories.

4) Final dividend subject to shareholder approval at the AGM on 16 November 2021.

Outlook

The macro outlook remains uncertain, in particular regarding supply chain disruption and inflationary pressures from freight and driver shortages. In line with the comments made at our Preliminary Results in September, we continue to work closely with our long-term suppliers and partners to mitigate the impact of these factors within our supply chain.

Whilst we are not immune to the challenges being widely reported, we feel well placed relatively to manage them. In particular, we have good stock levels across our stores, warehouses and supplier partners, a low proportion of seasonal ranges within our product offer, and also benefit from a higher propensity for customers to substitute products within homewares categories, given our broad range.

Sales growth in the first quarter of the new financial year has been encouraging and we have seen continued outperformance versus the homewares market. In the absence of any significant change in consumer demand driven by further Covid-related lockdowns or other industry shortages, the Board expects that FY22 full year profit before tax will be in line with analysts’ recently increased consensus expectations(5).

5) Management understand the range of analysts’ estimates(which have been updated since the FY21 results on 8 September 2021) for FY22 PBT is £167-£190m, with consensus of £179m.

Nick Wilkinson, Chief Executive Officer, commented:

“We are pleased with our performance in the first quarter, with sales growth across all channels and continued market share gains, especially given the strength of the comparative period last year, which benefited from pent-up demand following the first UK lockdown.

“We continue to invest in enhancing our market leading proposition to win more customers who shop more frequently across Dunelm’s expanding range. For example, we have now developed a ‘my favourites’ functionality online, which is another step in getting closer to our customers and making their homewares shopping as easy as possible.

“In the current environment, our purpose to help customers create the joy of truly feeling at home feels increasingly relevant and we are excited about our plans to become the 1st choice for home for more UK shoppers.”

Source : Dunelm

Insight DIY always publishes the latest news stories before anyone else and we find it to be an invaluable source of customer and market information.

Don't miss out on all the latest, breaking news from the DIY industry