UK DIY News

MRI: Retail Footfall Rebounds in February

- Shoppers are visiting with intention as trips are concentrated around weekends, holidays and key occasions.

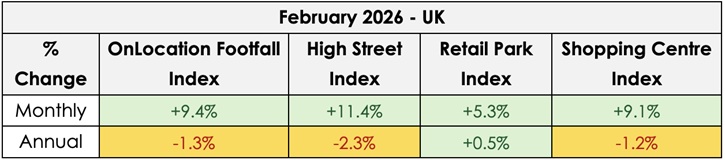

February delivered a strong month-on-month rebound for UK retail destinations, with total footfall rising +9.4% compared with January 2026. This was a welcome uplift, following the traditional slump that followed the festive period, and notably stronger than the same period last year when named storms and widespread travel disruption likely suppressed activity.

That said, the annual comparison remains subdued. Total footfall was -1.3% lower than February 2025, with challenging weather conditions likely tempering early momentum. What’s particularly interesting is the continued divide between weekday and weekend performance. Weekend footfall rose +1.9% year-on-year, while weekdays declined -2.7%, reinforcing a shift that’s been noted since November 2025. Midweek activity continues to feel the impact of hybrid working patterns, whereas weekends remain the anchor point for physical retail, likely driven by socialising, leisure-led visits and more intentional shopping trips.

Retail parks were once again the standout performer and the only destination type to record year-on-year growth (+0.5%). In the first week of February, when heavy rain may well have contributed to a -3.9% drop in high street footfall week over week, retail parks noted a +1.4% uplift. Their resilience remains consistent as convenience, accessibility and free parking continue to resonate with shoppers, particularly during periods of poor weather. As cost-conscious consumers remain selective about trips, destinations that offer ease and efficiency are maintaining that competitive edge.

The February half-term once again proved to be an important catalyst for retail. In the lead up to the holiday, high street footfall rose by +9.4% week-on-week as families prepared for the school holidays and Valentine’s Day. Visits to high streets remained particularly strong on Valentines Day itself recording an impressive +18.4% uplift in footfall week on week and 23.9% year on year. The week of half term itself benefited historic towns and Central London as day trips increased, with footfall rising +8.9% and +7.9% respectively, week on week, during the holiday period. Wales stood out in particular, recording an +11.4% uplift in visits week on week and +9.9% year on year.

While activity naturally slowed in the final week as schools returned, most noticeably in shopping centres, the +11.7% (WoW) rebound in all UK retail destinations on the final Saturday of the month (aligning with payday weekend) suggests that consumer demand remains present. The key factor continues to be occasion-led triggers that give people a reason to visit.

Looking ahead, attention now turns to Mothers Day which falls mid-March and Easter in April however the school holidays may begin in the final week of March for many across the UK. Both dates are key in the calendar for driving retail footfall with Easter traditionally seen as one of the most significant trading periods outside of Christmas. With the calendar dates shifting once again, a pronounced spike in footfall is expected as the holiday approaches.

However, retailers are now operating against a more complex macroeconomic backdrop. As conflict in the Middle East deepens, travel restrictions and heightened geopolitical risk are prompting warnings about broader knock-on effects for consumer confidence and travel-dependent retail categories. City analysts and sector experts are flagging that the crisis could dent travel retail performance and deter discretionary spending as uncertainty persists in global markets.

At the same time, rising oil prices and volatility in energy markets may begin to filter through supply chains and pricing structures. While it is too early to quantify the impact, sustained uncertainty has the potential to influence consumer confidence and reinforce value-driven behaviour.

For now, the data highlights that consumers are still visiting physical destinations, but those visits are becoming more deliberate. Weekend concentration, weather sensitivity and occasion-led surges are defining current patterns. For retailers and landlords, the data reinforces what we’ve been seeing for some time. Footfall is there, but it’s increasingly concentrated; into weekends, into holiday periods and into destinations that make the trip feel worthwhile. The challenge isn’t simply driving volume; it’s understanding when and why people are choosing to visit and planning accordingly as we move into spring.

Source : MRI Software

Image : Jason Batterham / Shutterstock / 671551474

Insight provides a host of information I need on many of our company’s largest customers. I use this information regularly with my team, both at a local level as well as with our other international operations. It’s extremely useful when sharing market intelligence information with our corporate office.

Don't miss out on all the latest, breaking news from the DIY industry