UK DIY News

NIQ: Spending Stalls Post-Easter as Shoppers Anticipate Summer Deals

- Shoppers remain cautious ahead of the summer months as seasonal offers increase to 26% of sales

- An earlier than usual Easter resulted in a decline in unit sales (-3.6%) and visits (-4.7%) over the four weeks

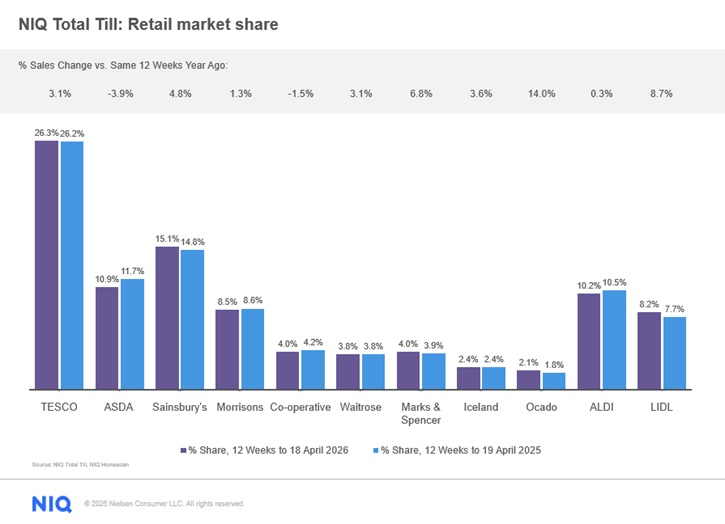

- Ocado (+14%), Lidl (+8.7% ) and M&S (+6.8%) remain the fastest growing retailers, while Asda (-3.9%) and Co-op (-1.5%) saw a decline in sales

Total Till sales at the UK major supermarkets were down (-0.2%) in the four weeks to 18th April after a surge in sales over the Easter bank holiday (+15.4%) according to new data released today by NielsenIQ (NIQ). Following earlier than usual Easter and Mothering Sunday offers, value sales then declined (-11.8%) during the week ending 18th April compared to Easter week 2025, due to both falling earlier in the calendar year by comparison.1

Across all channels, including convenience stores, shoppers spent a total of £16.9b (-2.1%) in the period with sales across the wider convenience channel particularly weak with a decline of -2.9%.

Unit sales also declined (-3.6%) over the four-week period partly due to less supermarket visits (-4.7%). Online remained the fastest growing channel with sales growth accelerating to +6.1%.

To help demand, retailers also focussed on seasonal offers and across all FMCG, the percentage of sales purchased on promotion accounted for 26% of sales, up from 24% a year ago.2 This included Easter meal staples such as fresh lamb and fresh salmon as the meat, fish and poultry super category saw the fastest growth with an increase in value sales of +3%. Continuing the focus for fresh foods and convenience, there was also more demand for fresh pasta and sauces (unit growth +8.4%), fresh dough and pastry (+5.4%) as well as fresh poultry (+3.1%).3

Shoppers focussed on restocking their pantries, with packaged grocery sales up (+3.1%) and units down only slightly (-0.5%). Shoppers also purchased more at supermarkets for entertaining and leisure around the Easter holiday with sales growth for toys (unit sales +5.2%), books (+4.9%) and cooking equipment (+2.9%).

Despite the Easter bank holiday celebrations, beer, wine and spirits sales were down (-5.7%) and units also declined (-7.2%). However ahead of the summer season, with events like Wimbledon and the World Cup, this category is set to see an increase in sales.

Over the 12 weeks, Total Till sales increased by +2.6% with Ocado seeing the fastest growth (+14%). Lidl (+8.7%) and M&S (+6.8%) also maintained growth. Tesco (+3.1%) and Sainsbury’s (+4.8%) also gained market share. Morrisons sales continue to improve (+1.3%) while Asda (-3.9%) and Co-op (-1.5%) sales continue to decline.

Mike Watkins, Head of Retailer and Business Insight at NielsenIQ, said: “Grocery ecommerce share dipped in the last four weeks, compared to earlier in the year, as this reflects shoppers’ preference for visiting stores to buy more fresh items for big seasonal celebration moments such as the Easter bank holiday weekend. However, despite this dip, online momentum remains strong as almost 1 in 3 households (29%) purchased online in the last four weeks 2, with unit growth up (+2%), and market share increasing to 13.9% of FMCG sales.”

Watkins continues: “The increase in promotions reflects the industry’s need to drive demand through offers and promotions to see an uplift in sales and visits. With two thirds of shoppers looking to buy extra for special events at stores 4 this helps drive footfall given that saving money is the keyconsumer mindset.”

He adds: “Shoppers will soon be under pressure from higher inflation so it will be important for retailers and brands to keep working together with relevant promotions to encourage shoppers to spend. This will be equally important as we head into another summer of sport – driven by the FIFA World Cup which is only six weeks away. This typically brings a strong feel-good factor among consumers, and with that comes enormous opportunities to capitalise on in the months ahead.”

Table: 12-weekly % share of grocery market spend by retailer and value sales % change

NIQ’s continuous panel of 30,000 GB households and its widest read of retailer performance is designed to measure household purchasing through major supermarkets, intended for in-home consumption and brought back into the home. It includes all food and drink, household, and personal care and an estimate of non-food spend (e.g. clothing, electrical, cards and stationery, newspapers & magazines, toys, music, general merchandise, etc.).

Unless otherwise stated all data is NIQ Homescan Total Till.

1 NIQ Scantrack Grocery Multiples

2 NIQ Homescan FMCG

3 NIQ Scantrack Total Coverage

4 NIQ Homescan Survey March 2026

Source : NielsenIQ

Image : sergeyryzhov / iStock / 517010420

Insight provides a host of information I need on many of our company’s largest customers. I use this information regularly with my team, both at a local level as well as with our other international operations. It’s extremely useful when sharing market intelligence information with our corporate office.

Don't miss out on all the latest, breaking news from the DIY industry