UK DIY News

SIG Posts Flat LFL Revenue In Half Year Trading Update

SIG plc, a leading supplier of specialist insulation and building products across Europe, today issues a trading update for the six months to 30 June 2023 , in advance of the release of its H1 results on 8 August 2023.

Key points

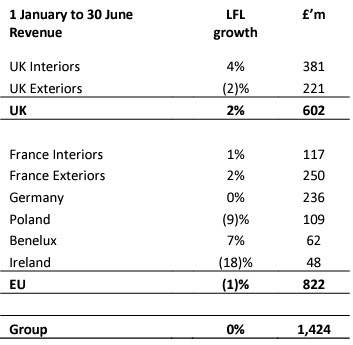

- Group revenue of £1,424m, representing flat like-for-like1 revenue versus prior year, reflecting volume declines offset by input price inflation

- Market conditions remained challenging and variable, with notably softer demand in May and June, particularly in Germany and France

- Underlying operating profit2 expected to be c.£33m, with early impact of productivity initiatives partially offsetting demand weakness and inflationary impact on operating costs

- Whilst timing of demand recovery remains uncertain, H2 profit is expected to benefit further from the ongoing productivity initiatives

- Consequently the Board continues to expect the Group to deliver full year underlying operating profit within the current range of market expectations3, but towards the lower end of that range

- Cash performance in the period in line with expectations, and reflecting the normal seasonal increase in working capital. The Board expects to report net debt at 30 June of £470m (post IFRS 16) and £176m (pre IFRS 16)

Trading Summary

Group LFL revenue was flat year-on-year in the period, with the continued positive tailwind from input price inflation being offset by lower volumes. The overall impact of inflation is estimated to have added c.9% to Group revenue growth in the period. As expected, price inflation moderated during H1 compared to the impact during 2022, as we annualise some of the significant prior year price increases. Reported Group revenue was 5% higher in the period, including c.3% from acquisitions, together with c.2% in aggregate from movements on working days and exchange rates.

Market conditions were challenging through H1 across our geographies, including a notable softening in demand in France and Germany in the last two months. Volumes and market conditions were notably weaker in Poland and Ireland over the period as a whole, with both also coming up against especially strong prior year comparators.

Outlook

We expect weak and uncertain demand conditions throughout the rest of the year, along with a continued, but further moderating, revenue tailwind from input price inflation. Whilst trading in recent weeks leads us to be more cautious as to the timing of any broad-based improvement in demand conditions, the second half will benefit from ongoing productivity initiatives as well as an expected profit on one specific property move. Consequently, the Board continues to expect the Group to deliver full year underlying operating profit within the current range of market expectations, but towards the lower end of that range.

Notwithstanding short-term market weakness, we continue to progress the strategic and operational initiatives which underpin our ambition for the Group. As a European market leader in the supply of specialist insulation, and with 80% of the Group's sales covering insulation and the wider building envelope, we are well-positioned to benefit from long-term structural growth drivers, notably sustainable construction and decarbonisation of buildings. We also remain confident in our ability to further improve our market positions, and to continue to improve our profitability when market conditions recover.

1. Like-for-like is defined as sales per working day in constant currency, excluding completed acquisitions and disposals

2. Underlying represents the results before Other items. Other items relate to the amortisation of acquired intangibles, impairment charges, profits and losses on agreed sale or closure of non-core businesses and associated impairment charges, net operating profits and losses attributable to businesses identified as non-core, net restructuring costs, and other non-underlying profits or losses.

3. Company collated analyst expectations is for Full Year 2023 underlying operating profit (EBIT) of £74.2m, within a range of £65.3m to £84.0m, as at 4 July 2023

Source : SIG plc

Insight DIY always publishes the latest news stories before anyone else and we find it to be an invaluable source of customer and market information.

Don't miss out on all the latest, breaking news from the DIY industry